|

| Image: Moneybestpal.com |

Asset valuation is the process of figuring out the fair market worth of an asset, such as stocks, bonds, real estate, or commodities. Because it has an impact on resource allocation, risk and return assessment, and adherence to accounting rules and regulations, asset valuation is significant to investors, businesses, and regulators.

There are different methods and approaches for asset valuation, depending on the type, purpose, and context of the asset. Some of the common methods are:

- Market approach: This approach calculates the asset's worth using the market values of comparable or related assets. For instance, by examining the costs of comparable homes in the same neighborhood or region, one might determine the value of a house.

- Income approach: This approach calculates the asset's present value using the anticipated future cash flows or income it will produce. A bond's value, for instance, can be calculated by applying a suitable interest rate to future coupon payments and principal repayment.

- Cost approach: This method uses the cost of creating or replacing the asset to estimate its value. For example, the value of a machine can be estimated by adding up the costs of labor, materials, and overheads involved in its production or acquisition.

- The asset's attributes and qualities, including its nature, maturity, liquidity, riskiness, cash flow structure, etc.

- The valuation's purpose and context, including whether it is being done for investments, reporting, taxes, regulations, etc.

- Data and information about the asset and its market, including historical prices, volumes, trends, and projections, are both readily available and of high quality.

- the methods and assumptions used to project the asset's future cash flows or income, including growth rates, discount rates, inflation rates, etc.

- Changes in inputs and assumptions are a result of the valuation's sensitivity and uncertainty.

Stock Valuation

|

| Image: Moneybestpal.com |

These ratios were used to construct an average relative valuation multiple for BlackRock's shares using a weighted average of its peers' multiples. For example,

|

| Image: Moneybestpal.com |

The estimated fair value per share of BlackRock was then calculated by multiplying this average multiple by the company's profits per share (EPS), book value per share (BVPS), or sales per share (SPS). For example,

|

| Image: Moneybestpal.com |

To calculate BlackRock's intrinsic value per share for the income approach, utilize a discounted cash flow (DCF) model based on the company's anticipated future free cash flows (FCF). Using historical growth rates, margins, and capital expenditure data, BlackRock's FCF was projected for the following five years. For example,

|

| Image: Moneybestpal.com |

The weighted average cost of capital (WACC), which represents BlackRock's minimum acceptable rate of return for its investors, is then applied to these FCFs. Based on its capital structure, cost of debt, and cost of equity, BlackRock's WACC is projected to be 8%. For example,

|

| Image: Moneybestpal.com |

|

| Image: Moneybestpal.com |

The enterprise value (EV), which is the total value of BlackRock's business, is calculated as the present value of FCF plus terminal value. Subtract BlackRock's net debt (total debt less cash and equivalents) from its EV to obtain the equity value. Divide the equity value by the number of outstanding shares to find the fair value per share. For example,

|

| Image: Moneybestpal.com |

The average fair value per share based on the market approach and the income approach is $800.

Real Estate Valuation

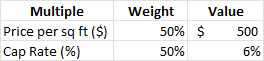

For the real estate properties let's try to value a commercial office building located in New York City. The property has a total area of 500,000 square feet, with an occupancy rate of 90% and an average rent of $50 per square foot per year.Both market and income approaches should be used to appraise this property. In the case of the market method, valuation metrics for the property (such as price per square foot, capitalization rate, etc.) were compared to those of comparable properties in the same market or region. For example,

|

| Image: Moneybestpal.com |

Calculate an average relative valuation multiple for the property based on these characteristics by averaging the multiples of its competitors. For example,

|

| Image: Moneybestpal.com |

To determine the property's estimated fair value, multiply this average multiple by the area or net operating income (NOI) of the building. For example,

|

| Image: Moneybestpal.com |

The average fair value based on these two multiples is $237.5 million.

To calculate the property's intrinsic value using the income approach, apply a discounted cash flow (DCF) model based on the anticipated net operational income for the property in the future (NOI). This can be accomplished by estimating the property's NOI over the course of the following ten years using its historical occupancy rate, rent growth rate, and operating expense data. For example,

|

| Image: Moneybestpal.com |

Asset Valuation: meaning, use, and why it matters

Asset Valuation is The process of figuring out the fair market worth of an asset, such as stocks, bonds, real estate, or commodities. In finance, the term matters because it turns a broad idea into something people can compare, question, and use in decisions. A short definition is useful for memory, but a practical explanation should also show when the concept appears, what assumptions sit behind it, and what changes after someone understands it.

For market concepts, separate signal from noise and understand what the measure can and cannot prove. This guide expands the concept into practical interpretation: what it means, how it works, how to avoid common mistakes, and how it connects with related MoneyBestPal topics.

How Asset Valuation works in practice

In practice, Asset Valuation usually appears inside a wider decision process. A company may use it while planning operations, an investor may use it while comparing opportunities, a lender may use it while judging risk, or a household may encounter it in budgeting, borrowing, saving, or taxes. The setting changes, but the purpose stays similar: the concept should improve judgment.

A useful framework is to identify three parts: the inputs, the interpretation, and the consequence. Inputs are the facts, numbers, terms, or assumptions that must be known first. Interpretation is what the concept tells you after those inputs are understood. Consequence is the action or risk that follows.

Example of Asset Valuation

Suppose an analyst, business owner, or student encounters Asset Valuation while reviewing a financial situation. The first step is not to jump to a conclusion. The better step is to ask what problem the concept is trying to clarify: timing, risk, value, legal responsibility, cash flow, incentives, or trade-offs.

If the concept affects risk, ask who bears the downside if assumptions are wrong. If it affects value, ask whether the value is based on cash flow, market price, accounting treatment, or future expectations. If it affects obligations, ask when responsibility starts, who must act, and what happens if conditions change.

Why Asset Valuation matters for financial decisions

Asset Valuation matters because financial decisions are rarely made with perfect information. People use financial concepts to simplify complex reality, but simplification can create false confidence if limitations are ignored. The best use of Asset Valuation is not mechanical. It should be combined with context, comparison, and judgment.

In business analysis, compare the concept with revenue quality, costs, margins, cash flow, competitive position, and management incentives. In personal finance, compare it with affordability, liquidity, time horizon, and downside protection. In investing, compare it with valuation, volatility, diversification, and opportunity cost.

Common mistakes when interpreting Asset Valuation

Mistake one: treating Asset Valuation as a standalone answer. Most finance terms are tools, not verdicts. They support a decision but do not replace broader analysis.

Mistake two: ignoring timing. A concept may look favorable in the short term while creating risk later, or unattractive now while improving long-term resilience.

Mistake three: comparing unlike situations. A metric or concept can mean one thing for a mature company and another for a startup, one thing in a stable economy and another during stress.

Mistake four: forgetting incentives. Whenever money, risk, control, or responsibility is involved, incentives shape how the concept works in reality.

How to use Asset Valuation wisely

To use Asset Valuation wisely, start with the definition and then move to the decision. Ask what problem it is supposed to solve. Next, identify the numbers, documents, assumptions, or market conditions needed. Then compare the interpretation with at least one alternative. Finally, ask what could go wrong if the conclusion is too optimistic, too narrow, or based on incomplete information.

This turns Asset Valuation from a memorized glossary term into a practical thinking tool. The goal is not just to know the phrase, but to understand how it changes decisions.

Checklist for applying Asset Valuation

Use this quick checklist before relying on Asset Valuation. First, confirm the source of the information and whether the definition matches the context. Second, separate facts from assumptions, especially when forecasts, estimates, legal duties, or market prices are involved. Third, compare the concept with a related measure so the conclusion is not based on one isolated phrase. Fourth, decide what action would change if the interpretation is correct. If nothing changes, the concept may be interesting but not decision-useful.

The checklist also helps prevent overconfidence. A term can sound precise while still depending on judgment, timing, data quality, and incentives. Good financial analysis treats Asset Valuation as one lens among several, not as a shortcut around careful thinking.

Limitations of Asset Valuation

The main limitation of Asset Valuation is that it can be misunderstood when taken out of context. Definitions are stable, but real situations are messy. Numbers can be incomplete, contracts can include exceptions, markets can change quickly, and people can respond to incentives in unexpected ways. That is why the same concept may lead to different decisions depending on cash flow, risk tolerance, time horizon, regulation, and available alternatives.

Another limitation is comparability. Two situations may use the same term while relying on different assumptions. Before comparing them, check whether the time period, measurement method, legal setting, or business model is similar enough for the comparison to be meaningful.

Which related MoneyBestPal guides should you read?

Frequently asked questions about Asset Valuation

Is Asset Valuation only relevant for finance professionals?

No. Professionals may use the term technically, but the underlying idea can affect everyday decisions about saving, borrowing, investing, taxes, budgeting, insurance, business, and risk management.

What is the best way to remember Asset Valuation?

Connect the definition to a real decision. Ask who uses it, what information they need, what conclusion they draw, and what risk remains afterward.

What should I compare Asset Valuation with?

Compare it with related measures, alternative scenarios, time period, incentives, and downside risk. A concept becomes more useful when it is tested against context instead of used in isolation.